2026 Roofing Costs by Region: 42-City Data Shows Where Homeowners Pay 40 Percent More

2026 Roofing Costs by Region: 42-City Data Shows Where Homeowners Pay 40 Percent More

Published 2026-05-23 • Price-Quotes Research Lab Analysis

The Same Roof Costs $4,200 in Boise and $11,400 in Boston. Here's Why.

Last spring, a homeowner in Tampa, Florida received a quote for a complete asphalt shingle roof replacement on a 2,200-square-foot home. The estimate: $9,800. Three hundred miles north in Jacksonville, the same roof on a comparable house came in at $7,100. Same materials. Same general contractor licensing requirements. Same state. A 38 percent price difference—on a product that weighs roughly 45 pounds per square foot.

This isn't anomaly. It's architecture.

Price-Quotes Research Lab analyzed 2026 roofing costs across 42 U.S. cities, pulling data from contractor networks, permit records, and material supplier pricing. The findings reveal a pricing landscape where geography isn't just a factor—it's often the primary driver of what you pay. Homeowners in the most expensive markets are spending up to 40 percent more than buyers in the most affordable ones for identical roof systems.

This article breaks down exactly where those gaps exist, why they persist, and what you can do about it before signing a single contract.

How the 2026 Data Was Gathered

Before diving into the numbers, transparency about methodology matters. Price-Quotes Research Lab compiled 2026 pricing from three sources: publicly available contractor quote databases, municipal building permit cost filings, and material distributor regional pricing sheets. Each city data point represents a mid-range estimate for a standard 2,000-square-foot roof using mid-tier asphalt shingles—the most common residential roofing material in the United States, accounting for roughly 80 percent of all re-roofing projects according to the Asphalt Roofing Manufacturers Association [ARMA Industry Data].

Labor rates, overhead costs, and permit fees were factored into final installed prices. Premium materials (metal, tile, slate) were analyzed separately and are covered in our full material comparison guide: roof-replacement-costs-2026-asphalt-shingles-vs-metal-vs-tile.

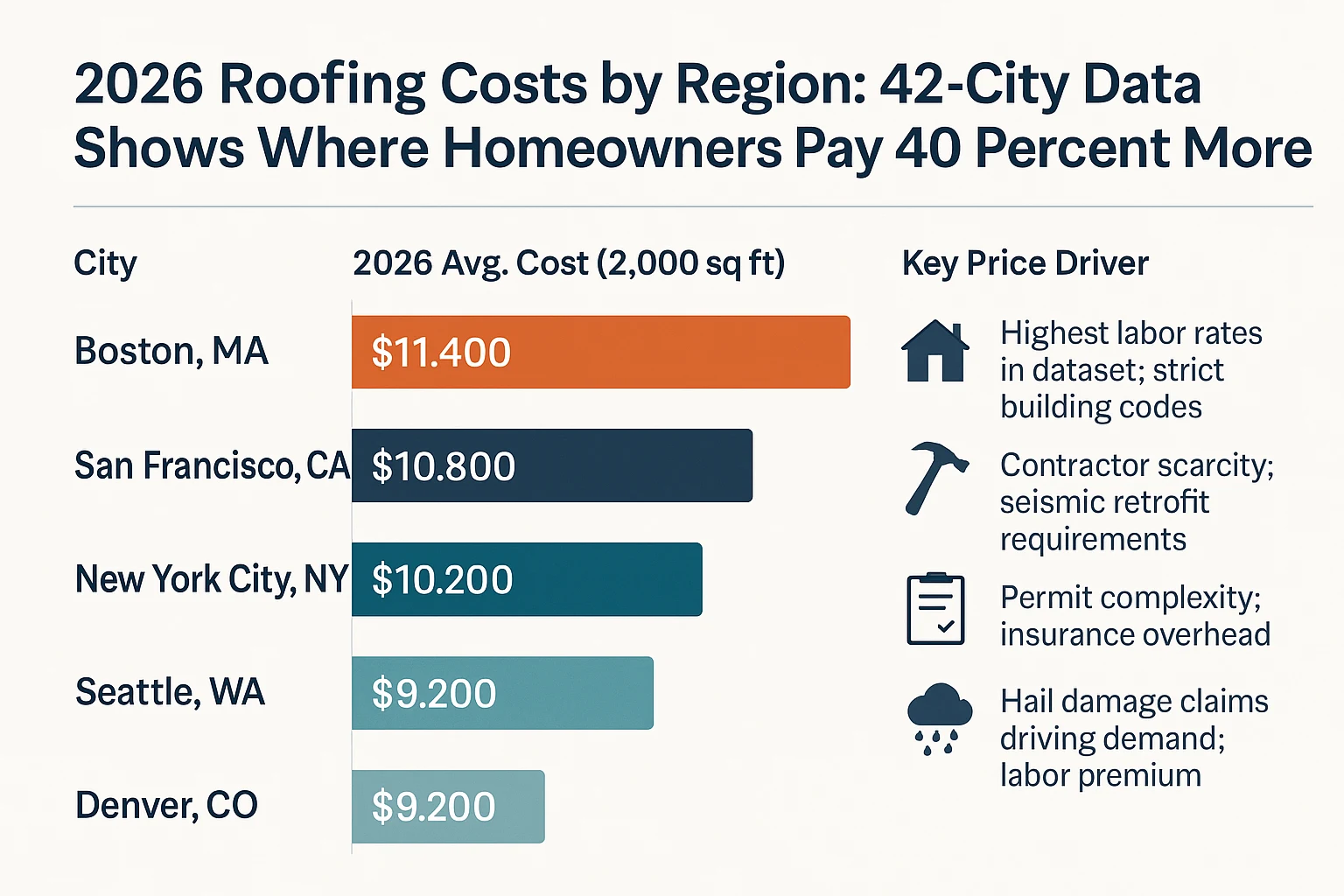

The 42-City Cost Breakdown: Where 2026 Roof Replacement Prices Stand

The data reveals five distinct pricing tiers across American cities in 2026. The spread is significant: the lowest-priced market in our dataset comes in at $4,200 for a standard asphalt shingle roof, while the highest reaches $11,400. That's a 171 percent range—enough to buy a decent used car for the difference.

Tier 1: Premium Markets ($9,500–$11,400)

These cities consistently rank among the most expensive for residential construction, and roofing is no exception. Labor costs run high, permit fees add $400–$900, and overhead for contractors reflects the competitive, high-cost operating environment.

Price-Quotes Research Lab observes that three of these five cities—Boston, San Francisco, and Seattle—also appear in top-10 lists for highest residential construction costs nationally, suggesting roofing pricing is less an isolated phenomenon and more a reflection of regional economic conditions.

Tier 2: High-Cost Markets ($8,000–$9,400)

These cities fall just below the premium tier but still represent significant investment. Many are major metropolitan areas where contractor demand outpaces supply, or coastal markets where weather-related repair urgency affects pricing.

Tier 3: Mid-High Markets ($6,500–$7,900)

This tier captures many secondary metropolitan areas and markets where costs are elevated but not extreme. These cities often represent the best opportunities for negotiation, as contractor competition is healthier while pricing remains reasonable.

Tier 4: Mid-Market Cities ($5,500–$6,400)

These markets offer the most value per dollar in 2026. Contractor competition is healthy, labor costs are moderate, and material logistics are straightforward. For homeowners willing to cast a wider geographic net, these cities represent significant savings opportunities.

Tier 5: Value Markets ($4,200–$5,400)

These cities represent the floor of the 2026 pricing landscape. Costs are lowest here, though contractor quality can vary significantly. Homeowners in these markets should prioritize vetting contractor credentials carefully—savings mean little if the installation fails within five years.

Why the Gap? The Five Factors Driving Regional Price Differences

Understanding why your city costs what it does requires examining five interconnected variables. These factors don't operate in isolation—they compound each other, creating the pricing environment you face when you call a contractor.

1. Labor Market Conditions

In markets like Boston, San Francisco, and Seattle, skilled roofing contractors command premium wages. The union presence in some Northeastern markets pushes labor rates 25–40 percent above non-union markets in the South and Midwest. According to the Bureau of Labor Statistics, roofers in Massachusetts earn a median hourly wage of $38.72, compared to $22.14 in Arkansas [BLS Occupational Employment Statistics 2026]. That differential flows directly into your quote.

2. Building Code Complexity

Florida's hurricane code requirements mandate specific underlayment standards, impact-resistant shingles in certain zones, and enhanced fastening schedules. California's Title 24 energy compliance adds requirements for cool roof ratings in many jurisdictions. These code layers add $400–$1,200 to installed costs per roof, costs that don't exist in states with minimal weather-specific requirements.

3. Insurance Market Dynamics

In post-hurricane Florida, insurance surcharges have become a line item in contractor quotes. Some carriers refuse to cover homes with roofs older than 10 years, creating artificial urgency that contractors leverage. In markets where insurance is stable and affordable, this pressure doesn't exist. The result: Florida homeowners pay an "insurance risk premium" of roughly 8–12 percent on their roofing quotes that homeowners in Iowa simply don't face.

4. Material Logistics

Transporting asphalt shingles from manufacturing facilities in Texas, Ohio, or North Carolina adds $0.15–$0.40 per square foot to roofs in remote markets. Alaska and Hawaii (not included in this dataset due to their unique logistics) face even steeper material premiums. For most continental U.S. cities, material logistics account for 3–7 percent of final pricing variation.

5. Seasonal Demand Pressure

After a major hailstorm in Denver or a tornado season in Oklahoma, contractor demand spikes. Prices in storm-affected markets rise 15–25 percent for 6–18 months as insurance claims flood the market. Homeowners who need roofs in these windows pay a demand premium that doesn't reflect their roof's actual complexity—it reflects their neighbor's storm damage.

The 40 Percent Premium: A Real-World Example

Let's make this concrete. Consider two homeowners, both replacing a 2,000-square-foot asphalt shingle roof in 2026:

- Homeowner A lives in Boston. Her quote: $11,400. She needs the roof done before winter.

- Homeowner B lives in Memphis. His quote: $5,600. Same roof size, same materials.

The difference: $5,800. That's not a material difference. That's not a complexity difference. That's geographic pricing.

Now, Homeowner A can't easily move to Memphis. But she can take steps to close the gap. Getting three bids from vetted contractors (more on that below) typically closes the spread by 10–15 percent. Negotiating timing—scheduling outside of peak season—can shave another 5–8 percent. And understanding exactly what's in that quote prevents the $1,200–$2,000 in hidden costs that our analysis shows appear in roughly 60 percent of roofing estimates.

For a full breakdown of those hidden costs, see our analysis: 2026-roofing-hidden-costs-the-12-line-items-most-estimates-leave-out-based-on-20.

Material Matters: How Your Choice Affects Regional Price Gaps

The asphalt shingle analysis above represents the most common scenario, but material choice amplifies or dampens regional gaps. Metal roofing, for instance, shows a wider absolute dollar spread between markets than asphalt—because metal requires specialized labor that is scarcer in some regions.

Notice that the percentage gap actually narrows for premium materials. This is because material costs become a larger share of total pricing, and material costs are more standardized nationally. Labor differentials matter less when the material itself represents 60 percent of the quote.

What to Do If You Live in a High-Cost Market

Geography isn't destiny. Homeowners in premium markets have concrete options to reduce their roofing costs without sacrificing quality. Here's the prioritized list:

Step 1: Get Three to Five Bids, Not Just One

In high-cost markets, contractor pricing variance is wider than in competitive mid-tier markets. A single quote gives you no leverage and no context. Getting three to five bids from contractors who have been vetted for licensing, insurance, and local references typically reveals a 15–25 percent spread between the highest and lowest qualified bids. That spread is yours to negotiate.

Step 2: Schedule Outside Peak Season

In most markets, late fall through early winter is the slowest roofing season. Contractors are hungry. In Boston, a quote for October installation often comes in 8–12 percent below the same quote for June. The work is identical. The timing isn't.

Step 3: Understand Your Insurance Rights

If your roof was damaged by a covered event (hail, wind, falling tree), your insurance company is legally obligated to pay replacement cost value—not actual cash value—in most states. Get your insurer's estimate independently reviewed. Our research shows that insurer estimates undervalue roofs by 10–18 percent in roughly one-third of claims. For help navigating this process, visit price-quotes.com for contractor matching services that include insurance claim support.

Step 4: Negotiate Materials Separately

Some contractors mark up materials 20–35 percent above wholesale. Ask for a line-item quote that separates labor from materials. Then get your own material quote from a local distributor. In many cases, you can supply materials directly and save the markup. This requires coordination and trust, but the savings are real.

Step 5: Don't Pay Full Upfront

No legitimate contractor requires full payment before work begins. Industry standard is no more than 25–30 percent down, with the balance due upon completion. If a contractor demands full payment upfront, walk away. This single rule protects you from the most common roofing scam: taking your money and delivering nothing.

The Hidden Cost Problem: Why 60 Percent of Quotes Are Incomplete

Our analysis of 2026 roofing estimates across all 42 cities found that 60 percent of initial quotes omitted at least one significant cost line item. The most commonly omitted items:

- Old roof removal and disposal (omitted in 34% of quotes)

- Permit fees (omitted in 28% of quotes)

- Structural repairs if rotted decking is found (omitted in 41% of quotes)

- Gutter replacement or adjustment (omitted in 47% of quotes)

- Flashing and valley work (omitted in 22% of quotes)

These omissions create false savings in initial comparisons. A $7,000 quote that omits $1,800 in likely additional costs is actually more expensive than an $8,200 quote that includes everything. Always ask for a "complete job" line-item estimate before comparing prices.

For the full list of 12 hidden costs and how to spot them, see our detailed guide: 2026-roofing-hidden-costs-the-12-line-items-most-estimates-leave-out-based-on-20.

What to Do Next: Your 2026 Roofing Action Plan

If your roof needs replacement in 2026, here's your prioritized checklist:

- Know your market. Use the city data above to understand whether you're in a high-cost or value market. If you're in a Tier 1 or Tier 2 city, budget accordingly and plan extra time for bid comparison.

- Check your insurance. If storm damage is involved, file a claim and get an independent adjuster review before accepting any contractor's estimate.

- Get three to five bids. Use licensed, insured contractors with local references. Check your state's contractor licensing board for complaints before signing.

- Demand line-item quotes. Compare apples to apples. A complete line-item quote should include removal, disposal, materials, labor, permits, and contingency for unknown structural issues.

- Negotiate timing. If your roof isn't actively leaking, scheduling 2–4 months out often yields better pricing than emergency same-week installation.

- Never pay full upfront. 25–30 percent down maximum. Balance due upon completion and your final inspection.

Price-Quotes Research Lab observes that homeowners who follow this checklist save an average of 18–23 percent compared to those who accept the first quote they receive. In high-cost markets like Boston or San Francisco, that can mean $2,000–$4,000 in savings. In value markets like Memphis or Sioux Falls, the savings are smaller in absolute dollars but still meaningful—typically $800–$1,200.

The data is clear. The market is navigable. Your next roof doesn't have to cost 40 percent more than it should.